Anderson-Sleath yield curves: latest and historical

Charles Coverdale

02 August 2026

Source:vignettes/yield-curves.Rmd

yield-curves.RmdThe Bank of England publishes daily fitted yield curves at all

maturities using the Anderson and Sleath (2001) smoothing methodology.

Five curves are produced: nominal gilt, real (index-linked) gilt,

implied inflation, overnight index swap (OIS), and the commercial bank

liability curve (BLC). Each is available in spot and

instantaneous-forward form, and in two segments: the standard

curve (half-year maturity steps out to 25 or 40 years) and the

separately fitted short end (monthly steps from one month to

five years), selected with segment = "short".

The default behaviour of boe_curve() returns the latest

published month, matching what most analysts need when they reach for

“today’s curve”. Pass from, to, or

frequency = "monthly" and the function switches to the BoE

historical archive, which extends back as far as 1979 for nominal

gilts.

Latest published month

latest <- boe_curve(curve = "nominal", measure = "spot")

#> ℹ Downloading yield curve archive from Bank of England

#> ✔ Downloading yield curve archive from Bank of England [402ms]

#>

range(latest$date)

#> [1] "2026-07-01" "2026-07-30"

range(latest$maturity_years)

#> [1] 0.5 40.0boe_curve() returns a long-format boe_tbl

with one row per (date, maturity) pair. Provenance is attached as an

attribute:

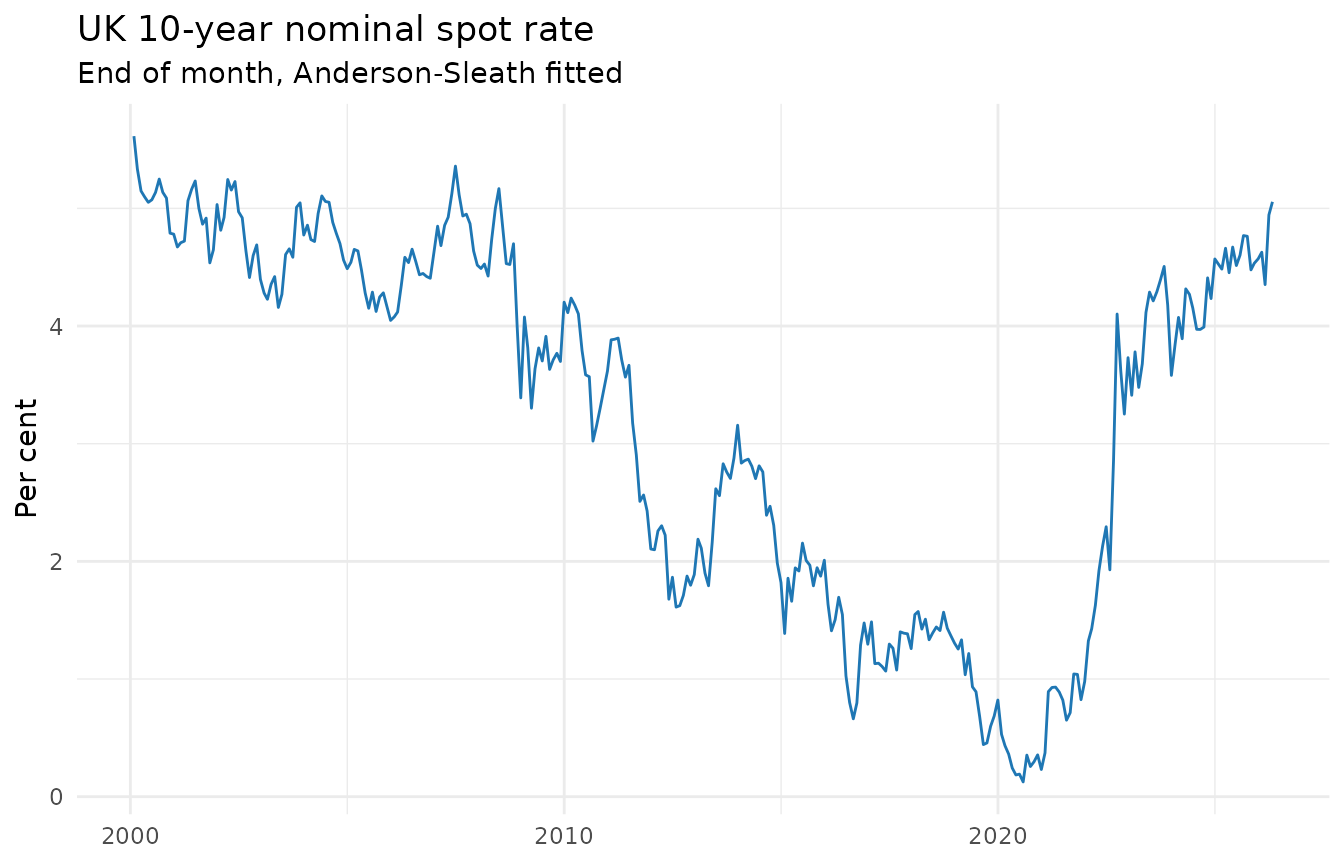

Historical: 10-year nominal spot rate since 2000

For time-series work, boe_curve_panel() reshapes the

long format into a wide panel with one column per pillar maturity.

End-of-month frequency is plenty for multi-decade work and keeps the

download small.

panel <- boe_curve_panel(

curve = "nominal",

measure = "spot",

frequency = "monthly",

from = "2000-01-01",

maturities = c(2, 5, 10, 20)

)

#> ℹ Downloading nominal monthly yield-curve archive from Bank of England

#> ✔ Downloading nominal monthly yield-curve archive from Bank of England [346ms]

#>

head(panel)

#> # BoE [boe_curve_panel]: 1 series [AS_NOMINAL_SPOT] · 6 obs · 2000-01-31 to 2026-06-30 · freq=monthly

#> date m2 m5 m10 m20

#> 1 2000-01-31 6.474909 6.286147 5.613887 4.478985

#> 2 2000-02-29 6.302563 6.010255 5.334982 4.363222

#> 3 2000-03-31 6.273430 5.857503 5.147789 4.349529

#> 4 2000-04-30 6.069206 5.704744 5.097727 4.262276

#> 5 2000-05-31 6.136496 5.695847 5.051332 4.304463

#> 6 2000-06-30 5.942865 5.594983 5.073053 4.379719

if (requireNamespace("ggplot2", quietly = TRUE)) {

ggplot2::ggplot(panel, ggplot2::aes(date, m10)) +

ggplot2::geom_line(colour = "#1f77b4") +

ggplot2::labs(

title = "UK 10-year nominal spot rate",

subtitle = "End of month, Anderson-Sleath fitted",

x = NULL, y = "Per cent"

) +

ggplot2::theme_minimal()

}

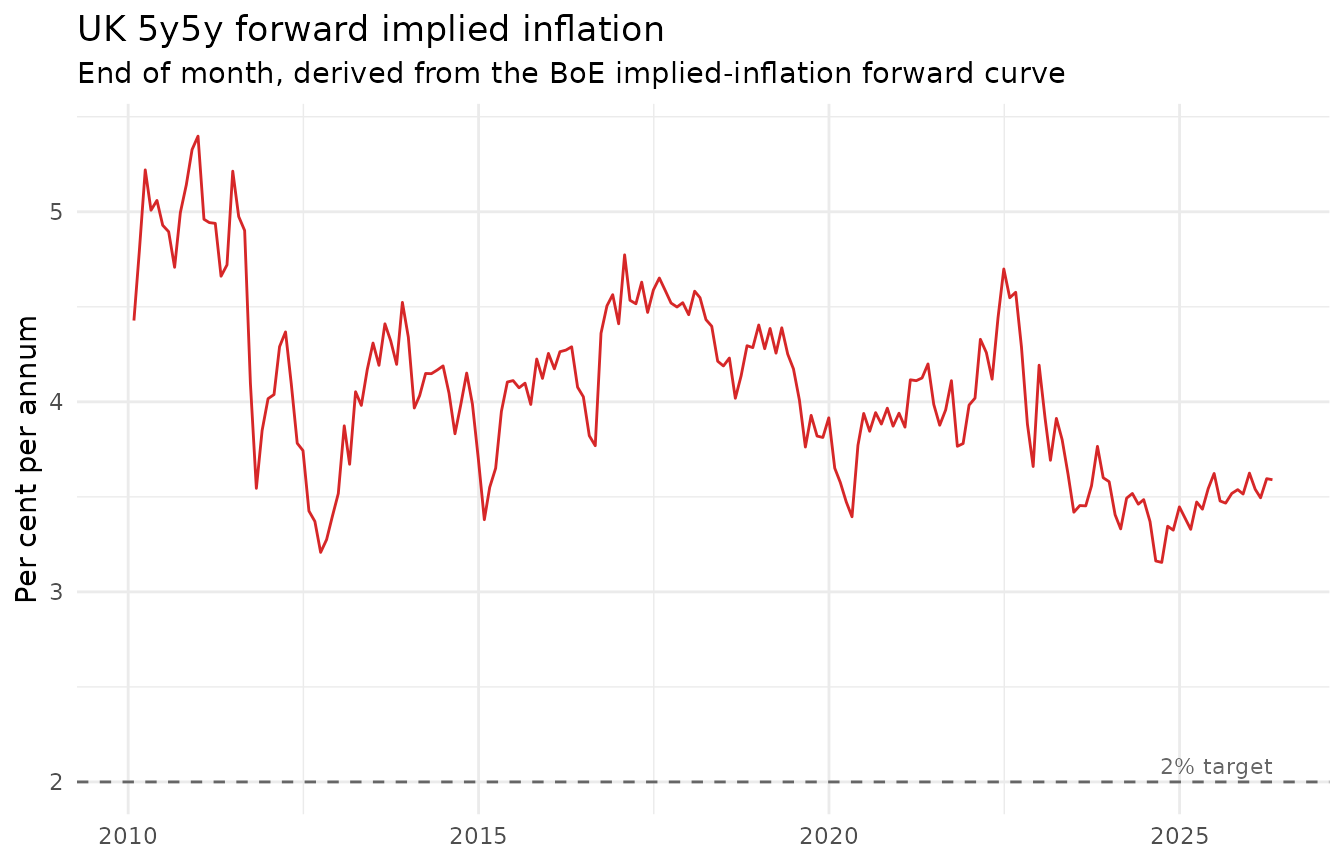

5y5y forward implied inflation

The 5y5y forward inflation rate (the average implied inflation rate over the second five-year horizon, five years from now) is a textbook medium-term inflation expectations measure. It comes straight off the implied-inflation forward curve.

inflation_fwd <- boe_curve_panel(

curve = "inflation",

measure = "forward",

frequency = "monthly",

from = "2010-01-01",

maturities = c(5, 10)

)

#> ℹ Downloading inflation monthly yield-curve archive from Bank of England

#> ✔ Downloading inflation monthly yield-curve archive from Bank of England [176ms]

#>

inflation_fwd$five_y_five_y <- (inflation_fwd$m10 * 10 -

inflation_fwd$m5 * 5) / 5

head(inflation_fwd[, c("date", "m5", "m10", "five_y_five_y")])

#> # BoE: 6 obs

#> date m5 m10 five_y_five_y

#> 1 2010-01-31 3.299640 3.863640 4.427640

#> 2 2010-02-28 3.401710 4.095848 4.789986

#> 3 2010-03-31 3.415668 4.318069 5.220470

#> 4 2010-04-30 3.458722 4.233360 5.007998

#> 5 2010-05-31 2.957608 4.008686 5.059764

#> 6 2010-06-30 2.779321 3.854157 4.928993

if (requireNamespace("ggplot2", quietly = TRUE)) {

ggplot2::ggplot(inflation_fwd, ggplot2::aes(date, five_y_five_y)) +

ggplot2::geom_line(colour = "#d62728") +

ggplot2::geom_hline(yintercept = 2.0, linetype = "dashed",

colour = "grey40") +

ggplot2::annotate("text", x = max(inflation_fwd$date),

y = 2.0, label = "2% target", hjust = 1, vjust = -0.5,

colour = "grey40", size = 3) +

ggplot2::labs(

title = "UK 5y5y forward implied inflation",

subtitle = "End of month, derived from the BoE implied-inflation forward curve",

x = NULL, y = "Per cent per annum"

) +

ggplot2::theme_minimal()

}

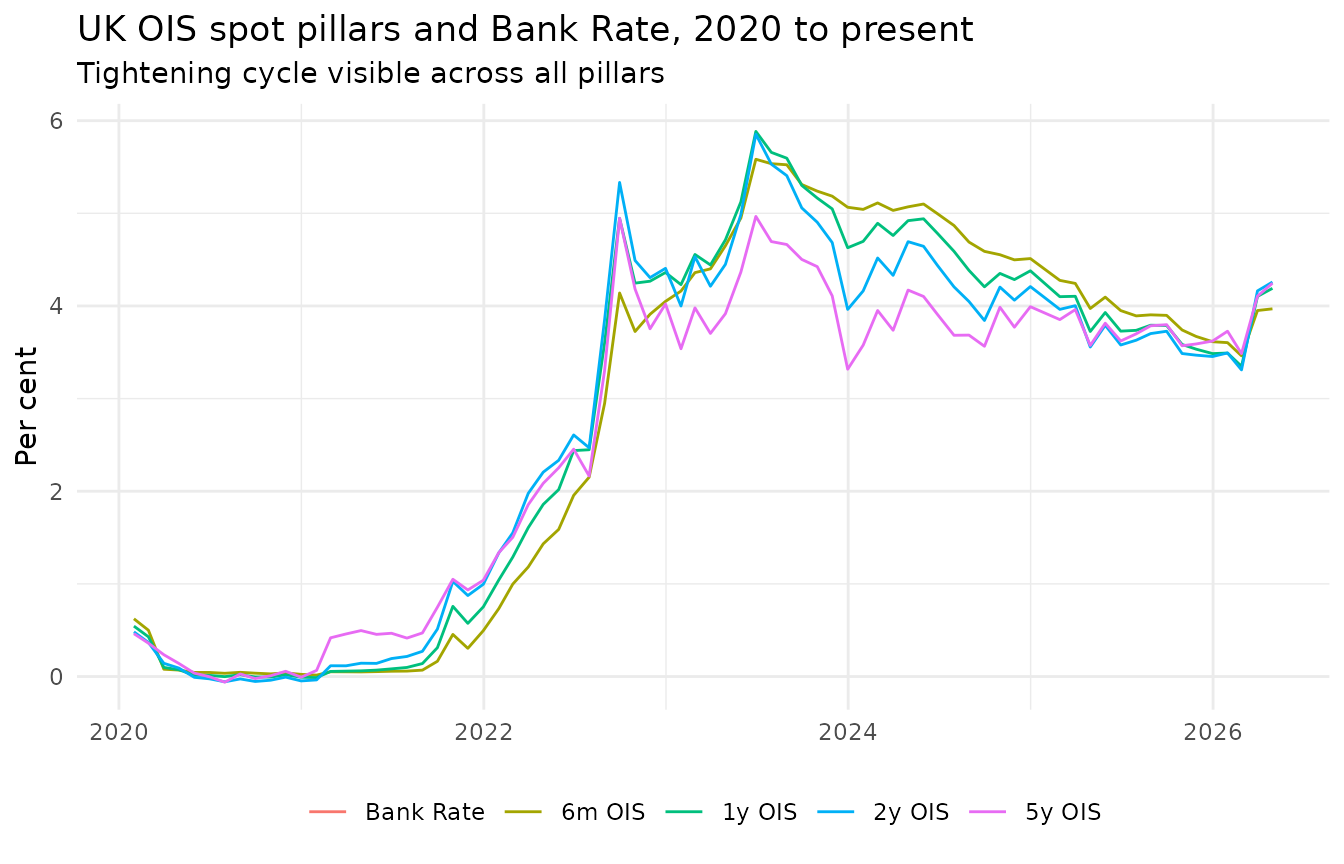

OIS curve evolution across the rate cycle

The OIS curve gives a market-implied path for Bank Rate. Comparing OIS spot pillars at MPC decision dates shows how expectations shifted through the 2022 to 2024 hiking cycle.

ois <- boe_curve_panel(

curve = "ois",

measure = "spot",

frequency = "monthly",

from = "2020-01-01",

maturities = c(0.5, 1, 2, 5)

)

#> ℹ Downloading ois monthly yield-curve archive from Bank of England

#> ✔ Downloading ois monthly yield-curve archive from Bank of England [234ms]

#>

mpc <- boe_mpc_decisions(from = "2020-01-01")

#> ℹ Downloading from Bank of England

#> ✔ Downloading from Bank of England [879ms]

#>

mpc <- data.frame(date = mpc$date, bank_rate = mpc$new_rate_pct)

merged <- merge(ois, mpc, by = "date", all.x = TRUE)

merged$bank_rate <- as.numeric(merged$bank_rate)

# carry the bank rate forward between MPC dates

for (i in seq_along(merged$bank_rate)) {

if (i > 1 && is.na(merged$bank_rate[i])) {

merged$bank_rate[i] <- merged$bank_rate[i - 1]

}

}

tail(merged)

#> date m0.5 m1 m2 m5 bank_rate

#> 72 2026-01-30 3.603969 3.491676 3.492607 3.727255 NA

#> 73 2026-02-27 3.461611 3.348672 3.309542 3.485201 NA

#> 74 2026-03-31 3.950747 4.102948 4.162256 4.106304 NA

#> 75 2026-04-30 3.968888 4.190262 4.258125 4.245096 NA

#> 76 2026-05-29 3.837568 3.955861 4.024661 4.078898 NA

#> 77 2026-06-30 3.810490 3.909603 3.983603 4.027876 NA

if (requireNamespace("ggplot2", quietly = TRUE)) {

long <- data.frame(

date = rep(merged$date, 5),

pillar = rep(c("Bank Rate", "6m OIS", "1y OIS", "2y OIS", "5y OIS"),

each = nrow(merged)),

rate = c(merged$bank_rate, merged$m0.5, merged$m1, merged$m2, merged$m5)

)

long$pillar <- factor(long$pillar,

levels = c("Bank Rate", "6m OIS", "1y OIS",

"2y OIS", "5y OIS"))

ggplot2::ggplot(long, ggplot2::aes(date, rate, colour = pillar)) +

ggplot2::geom_line() +

ggplot2::labs(

title = "UK OIS spot pillars and Bank Rate, 2020 to present",

subtitle = "Tightening cycle visible across all pillars",

x = NULL, y = "Per cent", colour = NULL

) +

ggplot2::theme_minimal() +

ggplot2::theme(legend.position = "bottom")

}

#> Warning: Removed 77 rows containing missing values or values outside the scale range

#> (`geom_line()`).

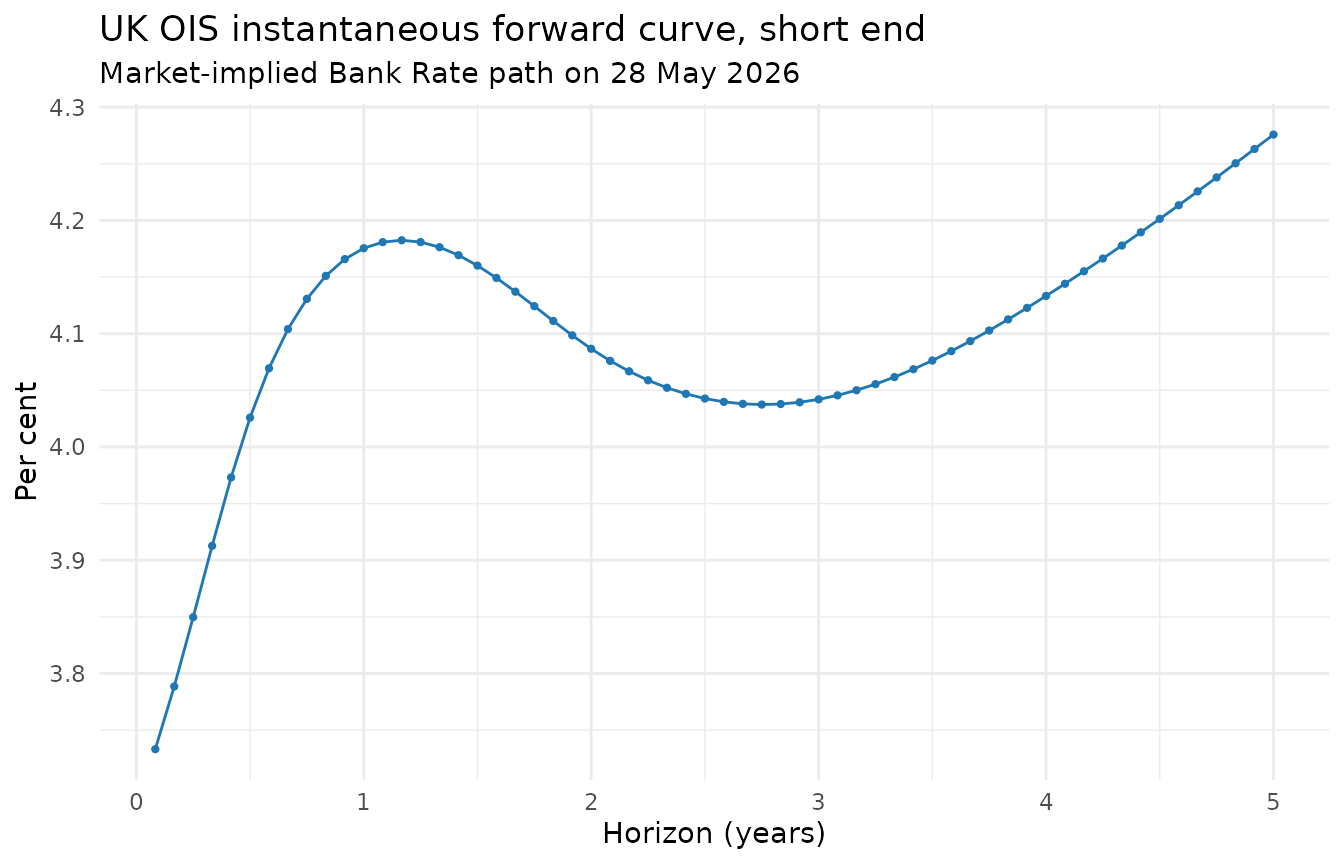

The short end of the curve

The standard curves step in half-years from 0.5 years out. For

near-term policy and money-market work the Bank fits a separate

short end at monthly maturities, from one month to five years.

Pass segment = "short" to boe_curve() or

boe_curve_panel() to reach it.

short <- boe_curve(curve = "nominal", measure = "spot", segment = "short")

#> ℹ Using cached yield curve archive

#> ✔ Using cached yield curve archive [6ms]

#>

range(short$maturity_years) # monthly grid, ~1/12 to 5 years

#> [1] 0.25 5.00The short end of the OIS forward curve is the cleanest market-implied path for Bank Rate: the instantaneous forward rate at each horizon, at monthly resolution. Here it is on the most recent published date.

ois_short <- boe_curve(curve = "ois", measure = "forward", segment = "short")

#> ℹ Using cached yield curve archive

#> ✔ Using cached yield curve archive [10ms]

#>

latest_day <- ois_short[ois_short$date == max(ois_short$date), ]

head(latest_day)

#> # BoE [boe_curve]: 1 series [AS_OIS_FORWARD_SHORT] · 6 obs · 2026-07-01 to 2026-07-30 · freq=daily

#> date maturity_years rate_pct

#> 1261 2026-07-30 0.08333333 3.729472

#> 1262 2026-07-30 0.16666667 3.802332

#> 1263 2026-07-30 0.25000000 3.875372

#> 1264 2026-07-30 0.33333333 3.942997

#> 1265 2026-07-30 0.41666667 4.004793

#> 1266 2026-07-30 0.50000000 4.064993

if (requireNamespace("ggplot2", quietly = TRUE)) {

ggplot2::ggplot(latest_day, ggplot2::aes(maturity_years, rate_pct)) +

ggplot2::geom_line(colour = "#1f77b4") +

ggplot2::geom_point(size = 0.8, colour = "#1f77b4") +

ggplot2::labs(

title = "UK OIS instantaneous forward curve, short end",

subtitle = paste("Market-implied Bank Rate path on",

format(max(ois_short$date), "%d %B %Y")),

x = "Horizon (years)", y = "Per cent"

) +

ggplot2::theme_minimal()

}

Short-end history goes back as far as the Bank published it: to 1979 for nominal gilts, and from 2016 for OIS. Where a period has no short-end sheet (early OIS, for instance), those dates are simply absent from the result rather than causing an error.

When to reach for the archive

| Question | Argument set |

|---|---|

| Today’s curve | none (default) |

| Last few years, daily | from = "2020-01-01" |

| Multi-decade panel for econometrics | frequency = "monthly", from = "1990-01-01" |

| Near-term policy-rate path, monthly detail | segment = "short" |

| Commercial bank liability curve |

curve = "blc" (always uses archive) |

Archive zips cache for 30 days by default; the latest-month zip

caches for 24 hours. Override with cache_ttl_h if you need

to force a fresh pull.

References

Anderson, N. and Sleath, J. (2001). New estimates of the UK real and nominal yield curves. Bank of England Working Paper No. 126. https://www.bankofengland.co.uk/working-paper/2001/new-estimates-of-the-uk-real-and-nominal-yield-curves