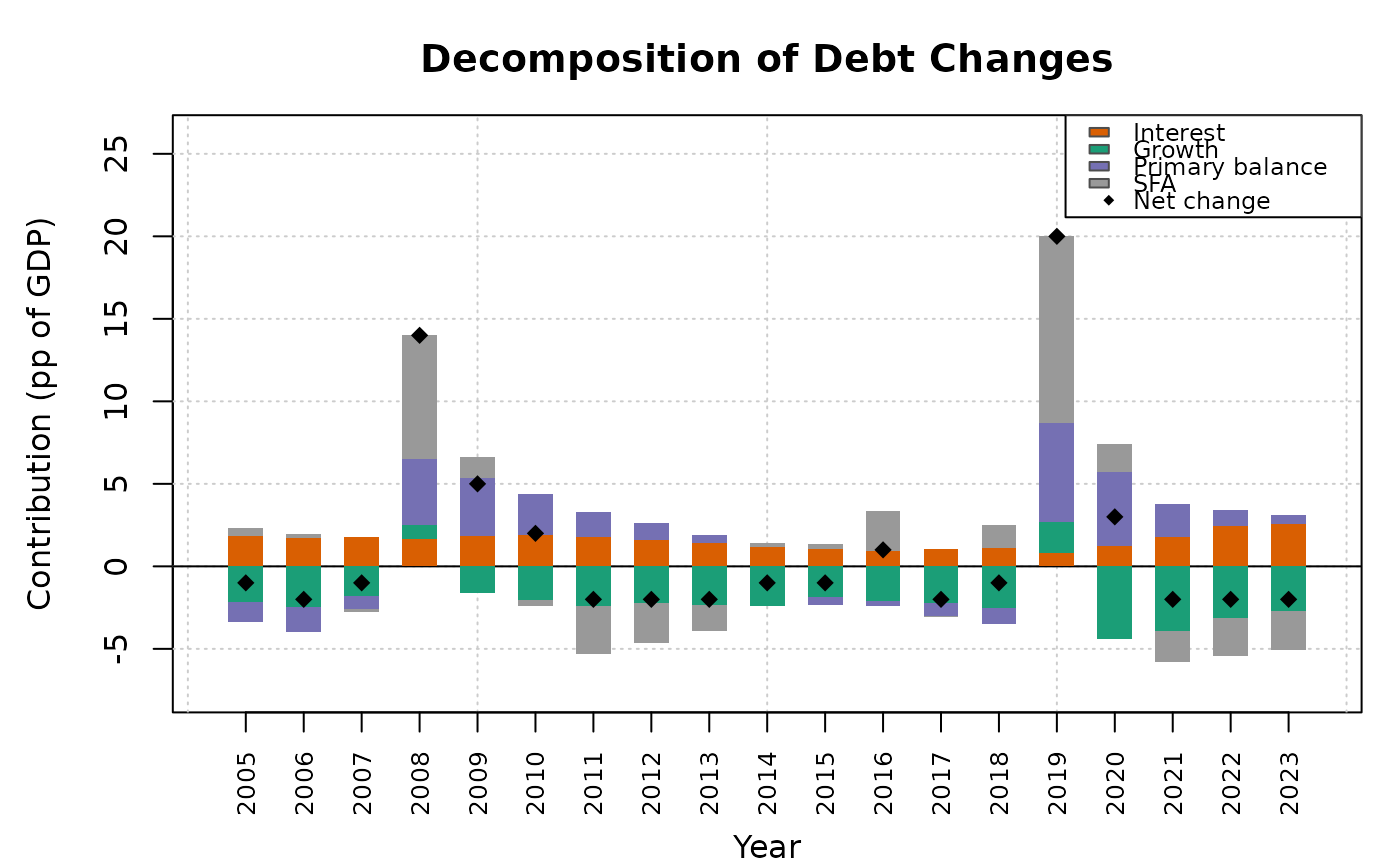

Breaks down observed year-on-year changes in the debt-to-GDP ratio into four components:

Arguments

- debt

Numeric vector of historical debt-to-GDP ratios.

- interest_rate

Numeric vector of effective interest rates on government debt. Must be the same length as

debt.- gdp_growth

Numeric vector of nominal GDP growth rates. Must be the same length as

debt.- primary_balance

Numeric vector of primary balance-to-GDP ratios (positive = surplus). Must be the same length as

debt.- years

Optional integer vector of year labels. Must be the same length as

debt. IfNULL(default), years are numbered sequentially.

Value

An S3 object of class dk_decomposition containing:

- data

A

data.framewith columnsyear,debt,change,interest_effect,growth_effect,snowball_effect,primary_balance_effect, andsfa.- years

The year labels used.

Details

Interest effect: \(r_t / (1 + g_t) \cdot d_{t-1}\)

Growth effect: \(-g_t / (1 + g_t) \cdot d_{t-1}\)

Primary balance effect: \(-pb_t\)

Stock-flow adjustment (residual): actual change minus the sum of the three identified components.

This is the standard decomposition used by the IMF (2013) and European Commission. The SFA residual captures privatisation receipts, exchange-rate valuation changes, below-the-line operations, and any measurement error.

References

Blanchard, O.J. (1990). Suggestions for a New Set of Fiscal Indicators. OECD Economics Department Working Papers, No. 79. doi:10.1787/budget-v2-art12-en

International Monetary Fund (2013). Staff Guidance Note for Public Debt Sustainability Analysis in Market-Access Countries. IMF Policy Paper.

Examples

d <- dk_sample_data()

dec <- dk_decompose(

debt = d$debt,

interest_rate = d$interest_rate,

gdp_growth = d$gdp_growth,

primary_balance = d$primary_balance,

years = d$years

)

dec

#>

#> ── Debt Decomposition ──────────────────────────────────────────────────────────

#> • Periods: 19 (2005–2023)

#> • Cumulative change: 24 pp

#> • Interest effect: 29.8 pp

#> • Growth effect: -39.5 pp

#> • Primary balance: 20.9 pp

#> • Stock-flow adj.: 12.8 pp

plot(dec)