Extracts the trend component from an inflation series using one of four methods: Hodrick-Prescott filter, Beveridge-Nelson decomposition, exponential smoothing, or centred moving average.

Arguments

- x

Numeric vector. An inflation time series.

- method

Character. One of

"hp","beveridge_nelson","exponential_smooth", or"moving_average".- frequency

Character. Data frequency:

"quarterly"(default),"monthly", or"annual". Used to set the HP filter lambda (whenlambda = NULL) and moving average window (whenwindow = NULL).- lambda

Numeric or

NULL. Smoothing parameter for the HP filter. IfNULL, defaults based onfrequency: 6.25 for annual, 1600 for quarterly (Hodrick and Prescott, 1997), or 14400 for monthly (Backus and Kehoe, 1992).- window

Integer or

NULL. Window size for the moving average method. Defaults to 4 for quarterly, 12 for monthly, or 3 for annual.

Value

An S3 object of class "ik_trend" with elements:

- trend

Numeric vector. The estimated trend component.

- cycle

Numeric vector. The cyclical component (original minus trend).

- method

Character. The method used.

- lambda

Numeric. HP filter lambda (if applicable).

- window

Integer. Moving average window (if applicable).

- alpha

Numeric. Exponential smoothing parameter (if applicable).

- original

Numeric vector. The original series.

References

Hodrick, R. J. and Prescott, E. C. (1997). "Postwar U.S. Business Cycles: An Empirical Investigation." Journal of Money, Credit and Banking, 29(1), 1-16.

Ravn, M. O. and Uhlig, H. (2002). "On Adjusting the Hodrick-Prescott Filter for the Frequency of Observations." Review of Economics and Statistics, 84(2), 371-376.

Examples

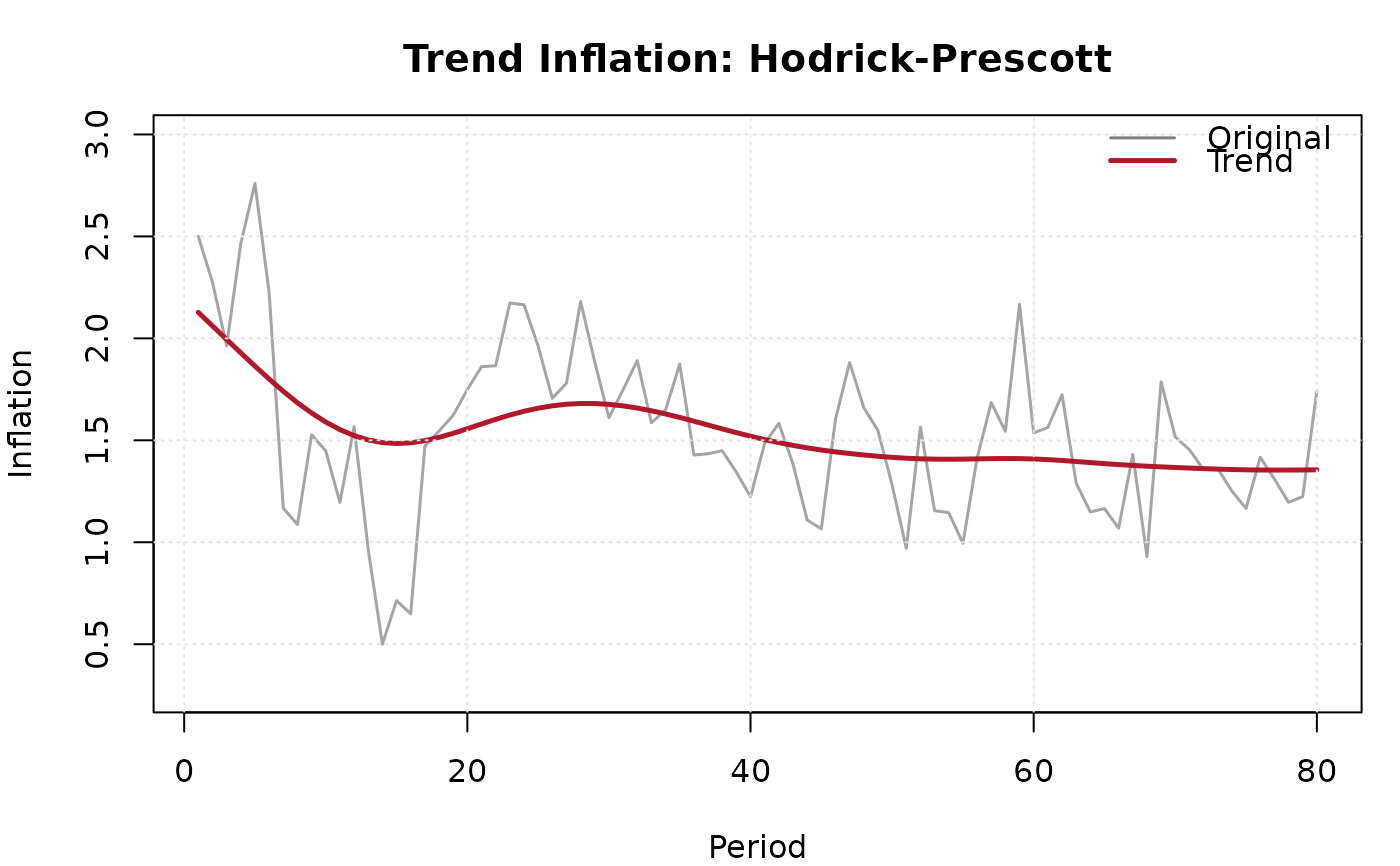

data <- ik_sample_data("headline")

tr <- ik_trend(data$inflation, method = "hp")

print(tr)

#>

#> ── Trend Inflation ─────────────────────────────────────────────────────────────

#> • Method: Hodrick-Prescott (lambda = 1600)

#> • Mean trend: 1.5261

#> • Cycle volatility (SD): 0.3405

#> • Observations: 80

plot(tr)

tr_ma <- ik_trend(data$inflation, method = "moving_average", window = 4)

print(tr_ma)

#>

#> ── Trend Inflation ─────────────────────────────────────────────────────────────

#> • Method: Moving Average (window = 4)

#> • Mean trend: 1.5298

#> • Cycle volatility (SD): 0.2118

#> • Observations: 80

tr_ma <- ik_trend(data$inflation, method = "moving_average", window = 4)

print(tr_ma)

#>

#> ── Trend Inflation ─────────────────────────────────────────────────────────────

#> • Method: Moving Average (window = 4)

#> • Mean trend: 1.5298

#> • Cycle volatility (SD): 0.2118

#> • Observations: 80