# Load in required packages

library(tidyverse) # Includes ggplot2, dplyr, purrr, stringr, etc.

library(ggridges) # For ridge plots

library(forecast) # Time series forecasting

library(ggrepel) # For better text label placement

library(viridis) # Color scales

library(readxl) # Excel file reading

library(lubridate) # Date and time manipulation

library(gapminder) # Gapminder data for examples

library(ggalt) # Additional ggplot2 geoms

library(scales) # Scale functions for ggplot2

library(readrba) # Get aus econ dataForecasting

So, we’ve got a time series dataset… but what is a reasonable forecast for how it might behave in the future?

Sure we can build a confidence interval (as we learned in the previous chapter) and figure out a reasonable value - but what about forecasting for multiple periods into the future?

That’s where we need to build models. Let’s load in some packages.

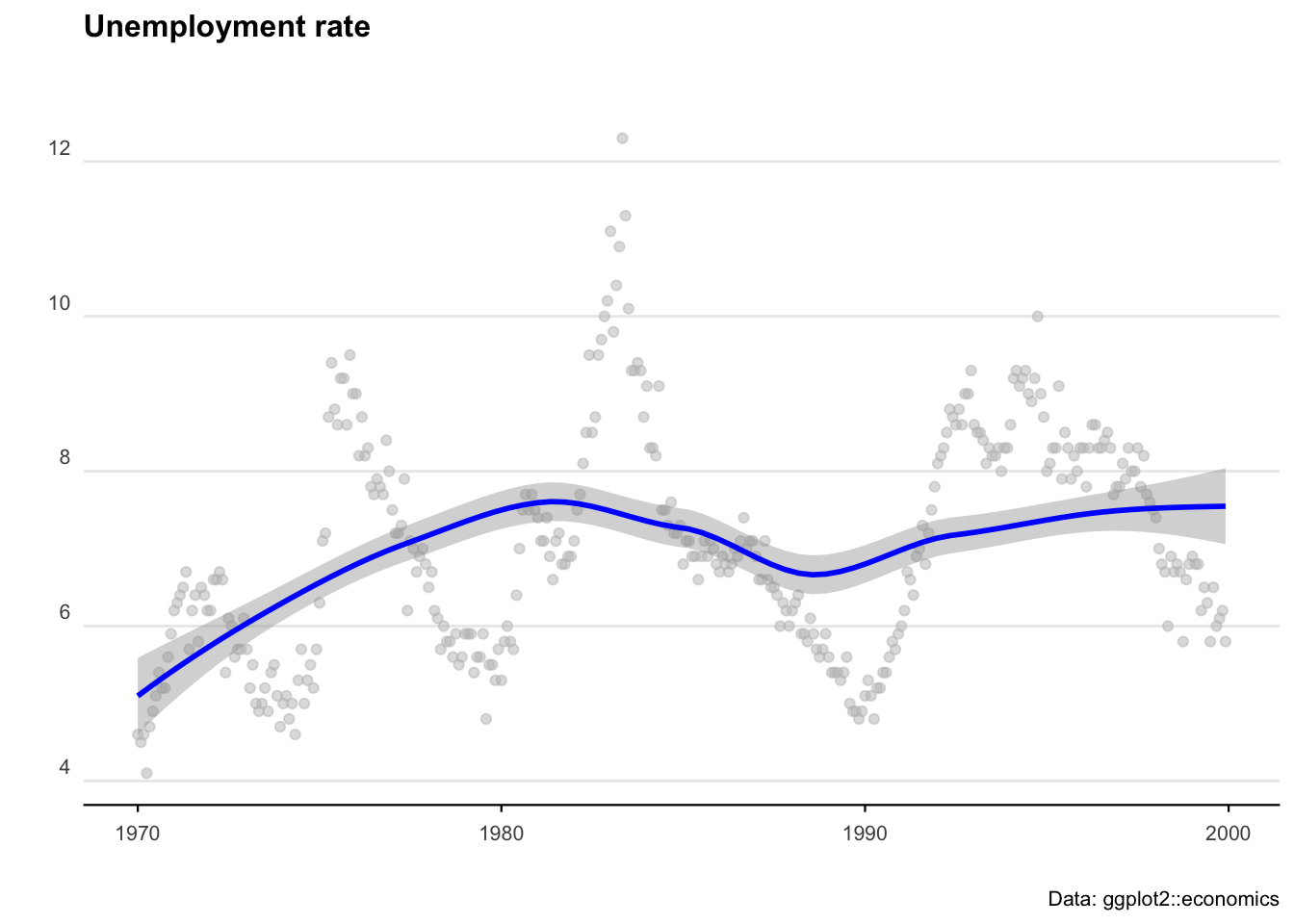

We’ll start with some pre-loaded time series data. The ggplot2 package includes a data set called ‘economics’ that contains US economic indicators from the 1960’s to 2015.

econ_data <- economics %>% dplyr::select(c("date", "uempmed"))

econ_data <- econ_data %>% dplyr::filter((date >= as.Date("1970-01-01") &

date <= as.Date("1999-12-31")))As a side note: We can also get Australian unemployment rate data using the readrba function.

aus_unemp_rate <- readrba::read_rba(series_id = "GLFSURSA")

head(aus_unemp_rate)Let’s plot the US data to see what we are working with.

ggplot(econ_data) +

geom_point(aes(x = date, y = uempmed), col = "grey", alpha = 0.5) +

geom_smooth(aes(x = date, y = uempmed), col = "blue") +

labs(

title = "Unemployment rate",

caption = "Data: ggplot2::economics",

x = "",

y = ""

) +

theme_minimal() +

theme(

plot.title = element_text(face = "bold", size = 12, margin = ggplot2::margin(0, 0, 25, 0)),

plot.subtitle = element_text(size = 11),

plot.caption = element_text(size = 8),

axis.text = element_text(size = 8),

axis.title.y = element_text(margin = ggplot2::margin(t = 0, r = 3, b = 0, l = 0)),

axis.text.y = element_text(vjust = -0.5, margin = ggplot2::margin(l = 20, r = -10)),

axis.line.x = element_line(colour = "black", size = 0.4),

axis.ticks.x = element_line(colour = "black", size = 0.4),

panel.grid.minor = element_blank(),

panel.grid.major.x = element_blank(),

legend.position = "bottom"

)

ARIMA

AutoRegressive Integrated Moving Average (ARIMA) models are a handy tool to have in the toolbox. An ARIMA model describes where Yt depends on its own lags. A moving average (MA only) model is one where Yt depends only on the lagged forecast errors. We combine these together (technically we integrate them) and get ARIMA.

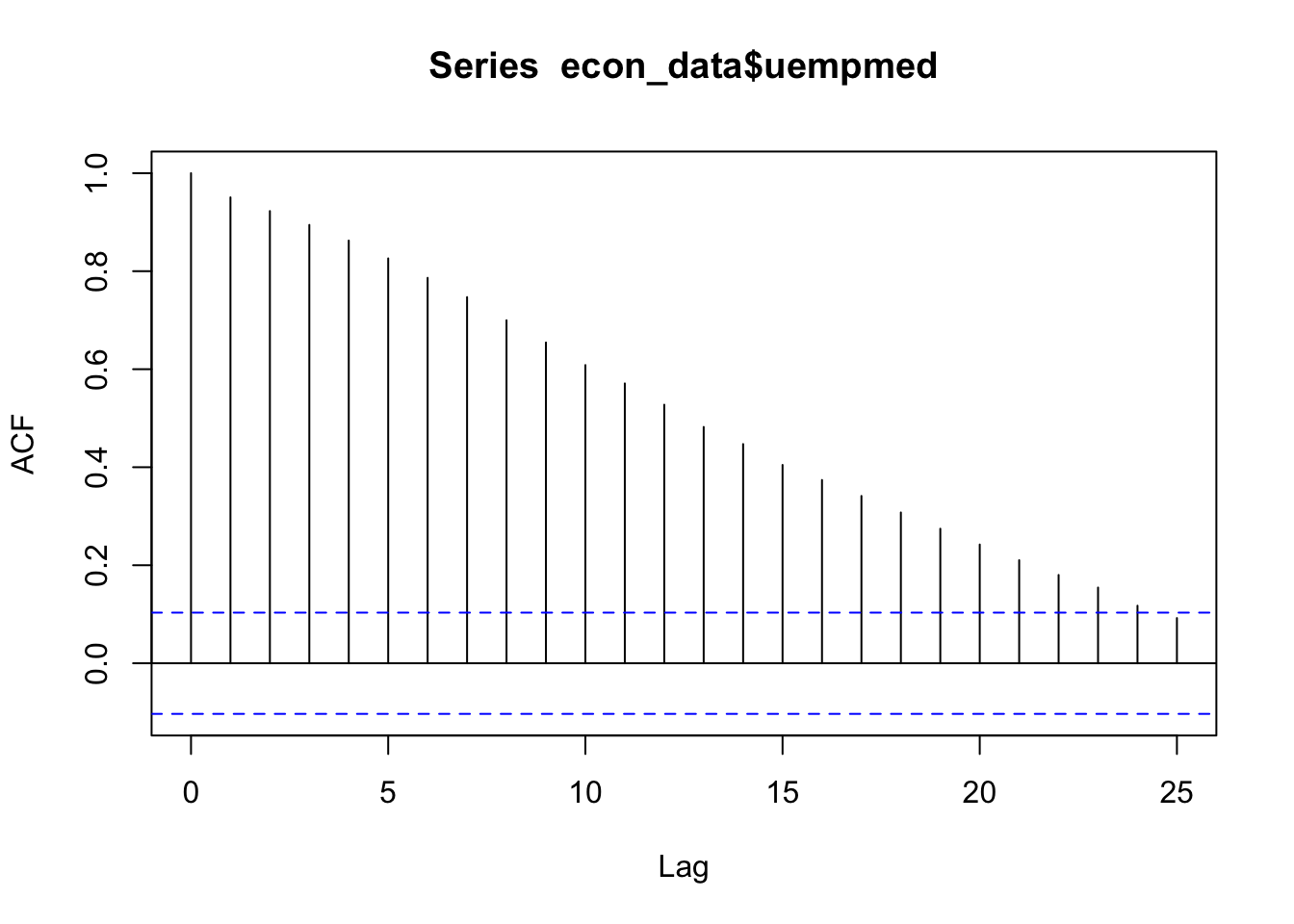

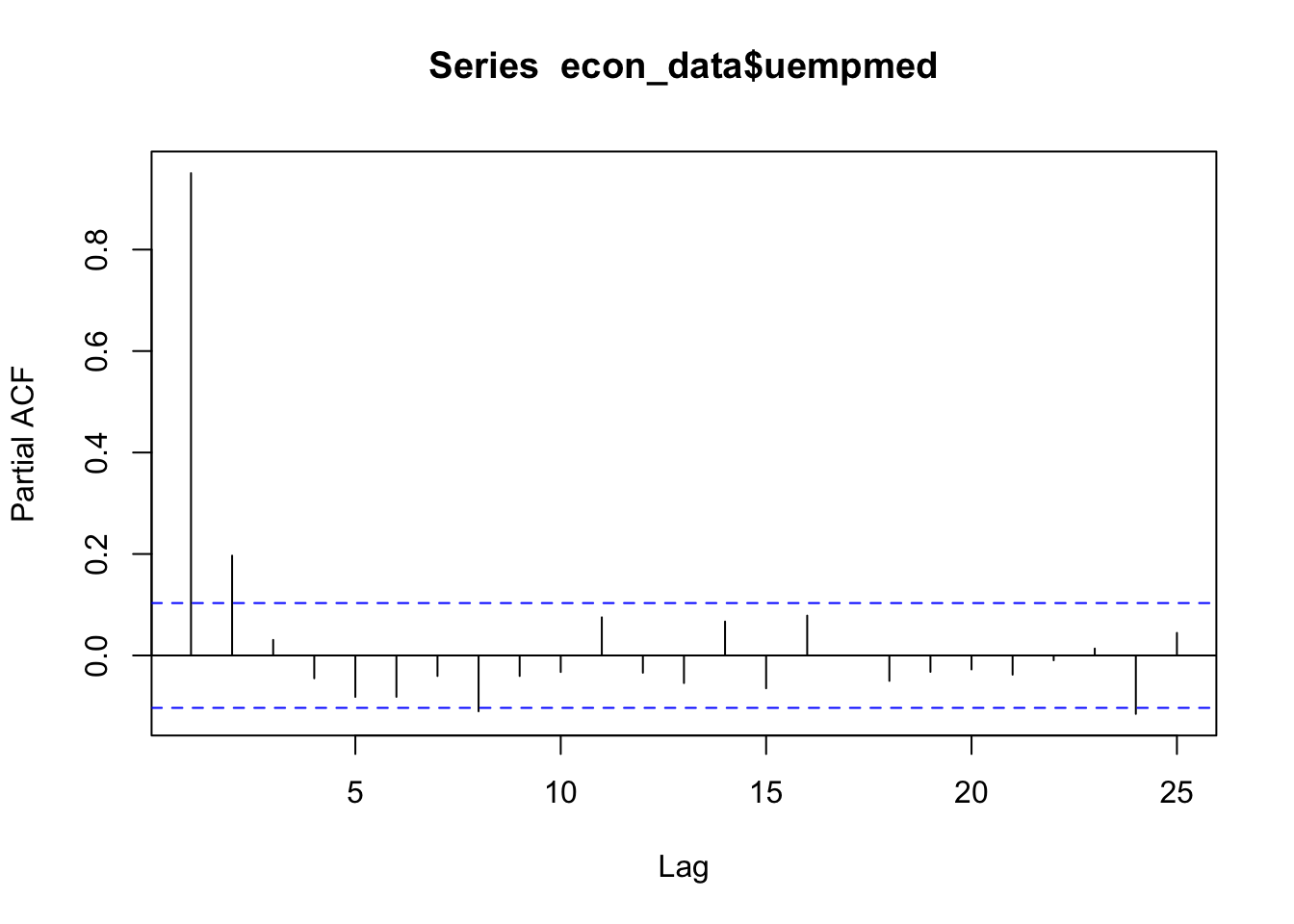

When working with ARIMAs, we need to ‘difference’ our series to make it stationary.

We check if it is stationary using the augmented Dickey-Fuller test. The null hypothesis assumes that the series is non-stationary. A series is said to be stationary when its mean, variance, and autocovariance don’t change much over time.

# Test for stationarity

aTSA::adf.test(econ_data$uempmed)

# See the auto correlation

acf(econ_data$uempmed)

# Identify partial auto correlation

pacf(econ_data$uempmed)

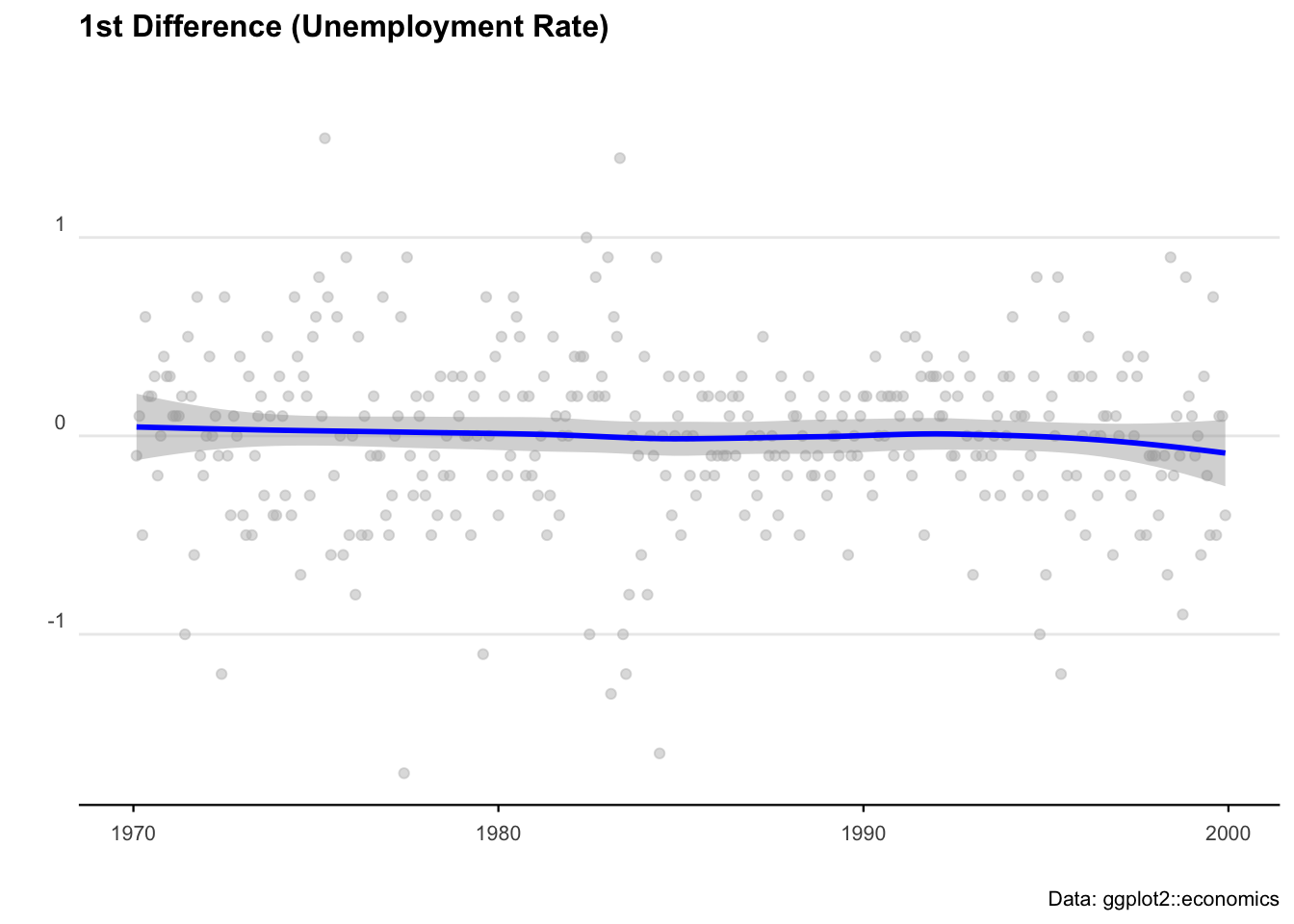

# Take the first differences of the series

econ_data <- econ_data %>% mutate(diff = uempmed - lag(uempmed))

# Plot the first differences

ggplot(econ_data, aes(x = date, y = diff)) +

geom_point(col = "grey", alpha = 0.5) +

geom_smooth(col = "blue") +

labs(

title = "1st Difference (Unemployment Rate)",

caption = "Data: ggplot2::economics",

x = "",

y = ""

) +

theme_minimal() +

theme(

legend.position = "bottom",

plot.title = element_text(face = "bold", size = 12, margin = ggplot2::margin(0, 0, 25, 0)),

plot.subtitle = element_text(size = 11),

plot.caption = element_text(size = 8),

axis.text = element_text(size = 8),

axis.title.y = element_text(margin = ggplot2::margin(t = 0, r = 3, b = 0, l = 0)),

axis.text.y = element_text(vjust = -0.5, margin = ggplot2::margin(l = 20, r = -10)),

axis.line.x = element_line(colour = "black", size = 0.4),

axis.ticks.x = element_line(colour = "black", size = 0.4),

panel.grid.minor = element_blank(),

panel.grid.major.x = element_blank()

)

# Fit an ARIMA model

ARIMA_model <- forecast::auto.arima(econ_data$uempmed)

# Display model summary and residual diagnostics

summary(ARIMA_model)

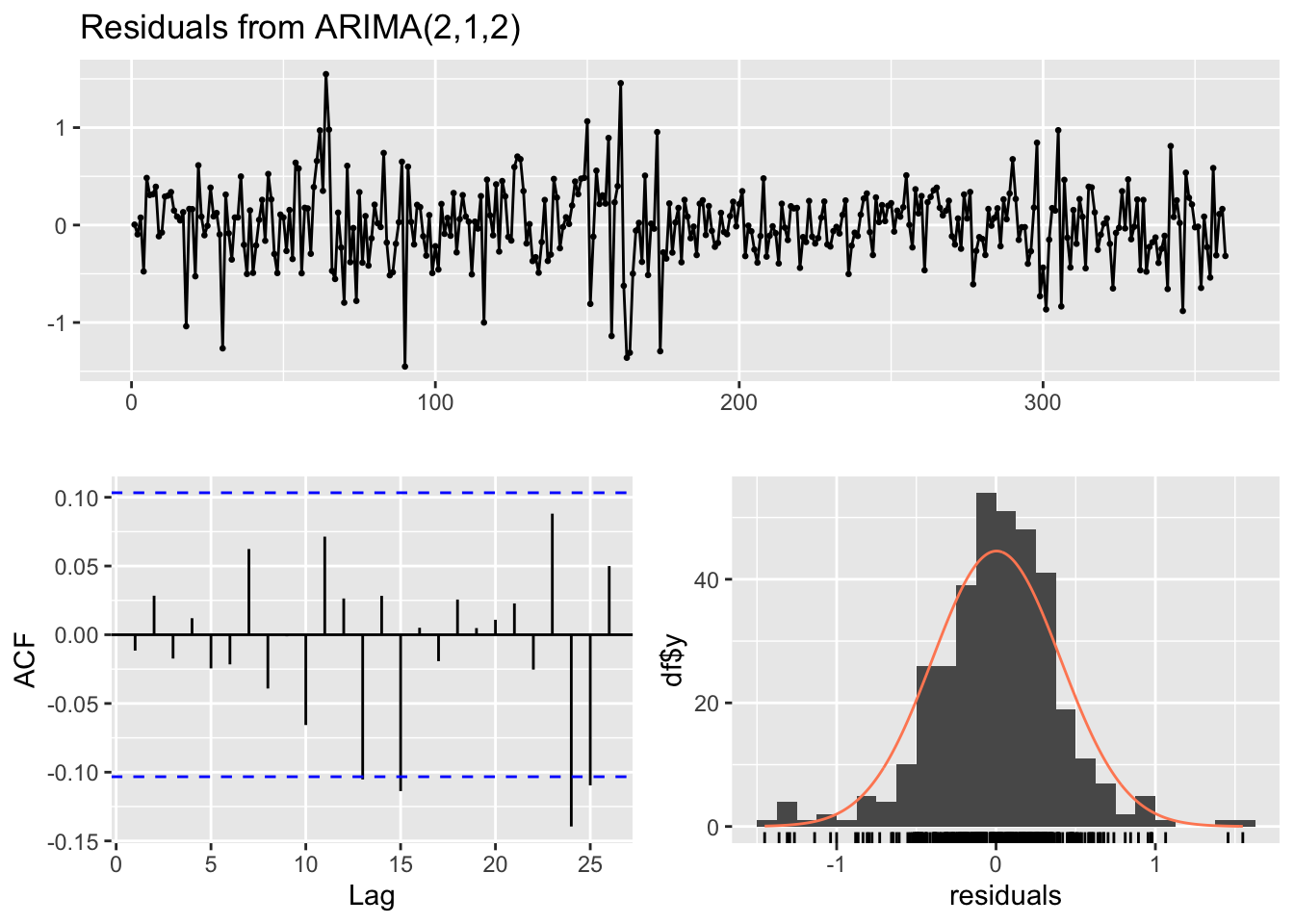

forecast::checkresiduals(ARIMA_model)

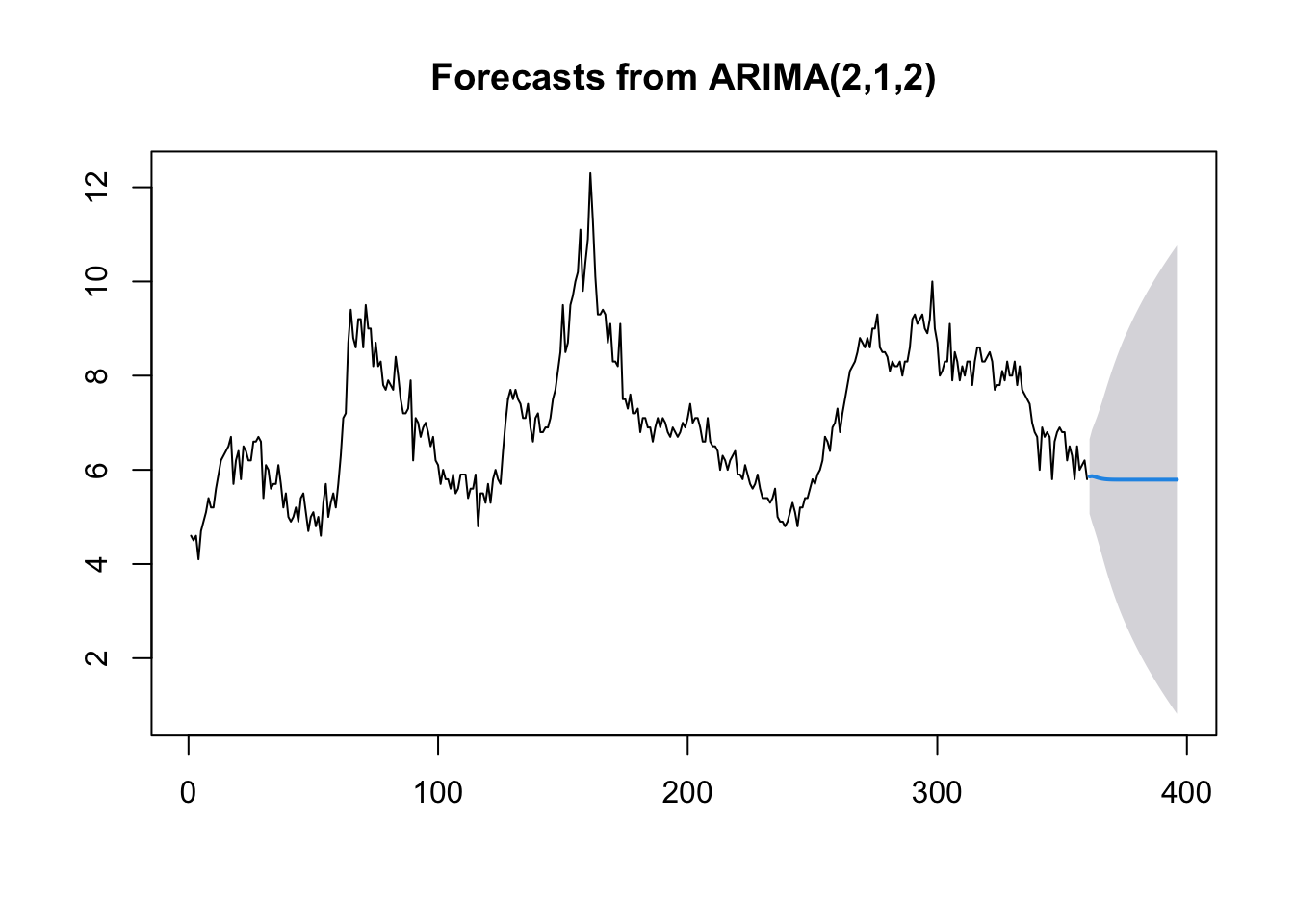

# Forecast for the next 36 time periods

ARIMA_forecast <- forecast::forecast(ARIMA_model, h = 36, level = c(95))

# Plot the forecast

plot(ARIMA_forecast)

Machine learning

There probably isn’t a hotter term this decade than ‘machine learning’. But the principles of getting machines to perform operations based on unknown inputs has been around for the best part of 100 years. ‘Figure it out’ is now an instruction you can give a computer — and with careful programming and enough data, we can get pretty close.

The modern standard for machine learning in R is tidymodels — a collection of packages that gives you a clean, consistent way to build, train, and evaluate models. It’s replaced the older caret package and is now the go-to approach for most R users doing ML work.

library(tidymodels)

library(ranger) # Fast random forest engineLinear regression with tidymodels

We know that a model is just any function (of one or more variables) that helps to explain observations. Let’s start with the simplest case: a linear regression predicting miles per gallon from horsepower using the mtcars dataset.

The nice thing about tidymodels is that every model follows the same pattern: define the model spec, bundle it into a workflow, fit it, then evaluate. Once you’ve learned it once, swapping between model types is trivial.

data(mtcars)

# Split into training (80%) and testing (20%) sets

set.seed(123)

mtcars_split <- initial_split(mtcars, prop = 0.8)

mtcars_train <- training(mtcars_split)

mtcars_test <- testing(mtcars_split)

# Define a linear regression model

lm_spec <- linear_reg() %>%

set_engine("lm")

# Bundle model + formula into a workflow

lm_workflow <- workflow() %>%

add_model(lm_spec) %>%

add_formula(mpg ~ hp)

# Fit on training data

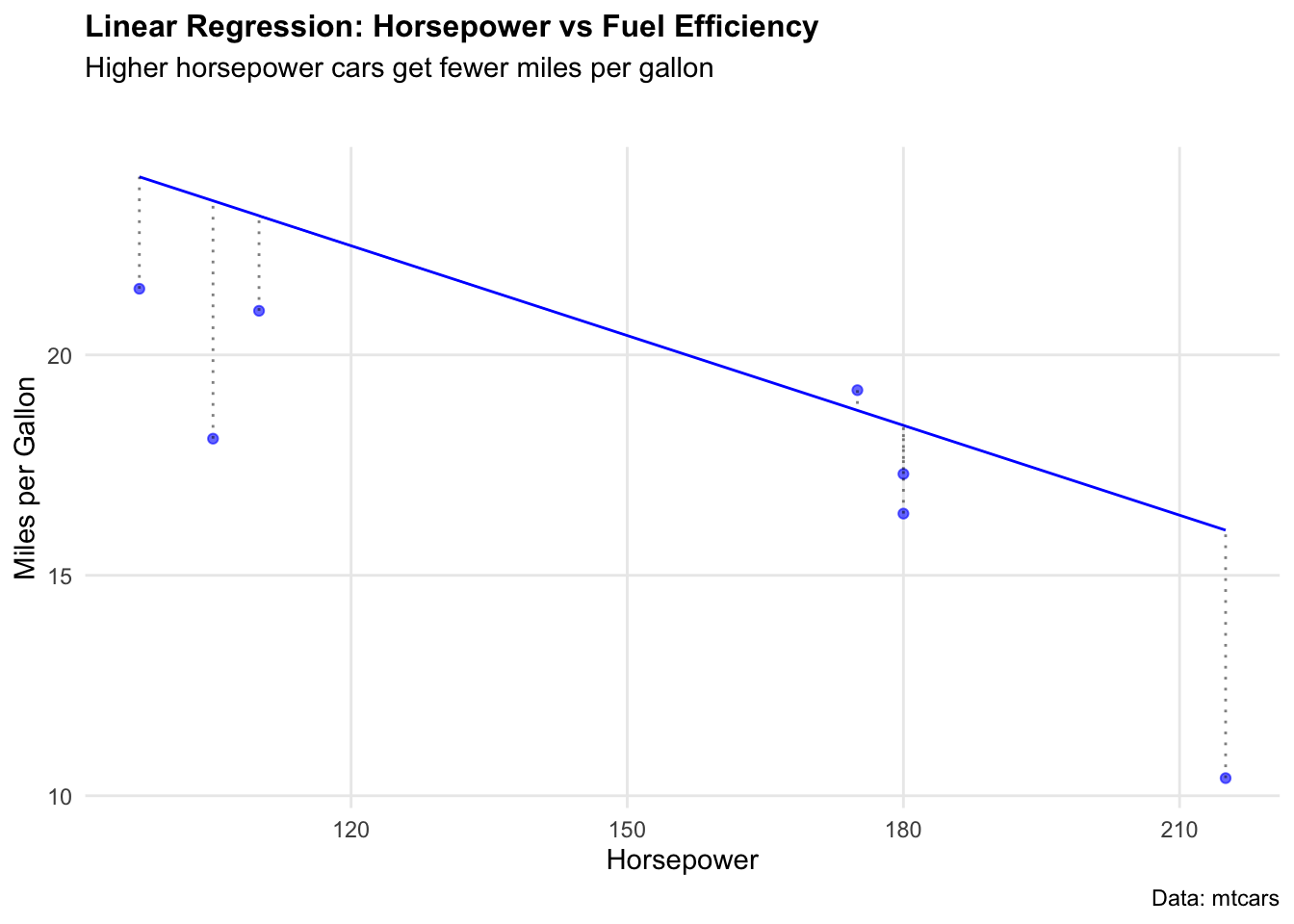

lm_fit <- lm_workflow %>% fit(data = mtcars_train)We can visualise how well the model fits by plotting predicted vs actual values.

# Generate predictions on test set

lm_preds <- predict(lm_fit, mtcars_test) %>% bind_cols(mtcars_test)

ggplot(lm_preds, aes(x = hp)) +

geom_point(aes(y = mpg), colour = "blue", alpha = 0.6) +

geom_line(aes(y = .pred), colour = "blue") +

geom_segment(aes(y = mpg, yend = .pred, xend = hp),

colour = "black", alpha = 0.5, linetype = "dotted"

) +

labs(

title = "Linear Regression: Horsepower vs Fuel Efficiency",

subtitle = "Higher horsepower cars get fewer miles per gallon",

caption = "Data: mtcars",

x = "Horsepower",

y = "Miles per Gallon"

) +

theme_minimal() +

theme(

plot.title = element_text(face = "bold", size = 12),

plot.subtitle = element_text(size = 11, margin = ggplot2::margin(b = 25)),

panel.grid.minor = element_blank()

)

To put a number on how well the model performed, yardstick (part of tidymodels) gives us RMSE, MAE, and R² in a single call — no manual calculations needed.

metrics(lm_preds, truth = mpg, estimate = .pred)Random forest

True machine learning takes this further by building many models across many parameter combinations to find the best predictors. Random forests are one of the most reliable approaches — they combine hundreds of decision trees and average their predictions, reducing overfitting.

We’ll use the Boston housing dataset to predict median home values (medv) from neighbourhood characteristics.

# Load Boston dataset

data("Boston", package = "MASS")

# Split into training (80%) and testing (20%)

set.seed(123)

boston_split <- initial_split(Boston, prop = 0.8)

boston_train <- training(boston_split)

boston_test <- testing(boston_split)We define a random forest model using rand_forest() with the ranger engine — a fast, modern implementation.

# Define random forest model

rf_spec <- rand_forest(trees = 500) %>%

set_engine("ranger") %>%

set_mode("regression")

# Bundle into workflow

rf_workflow <- workflow() %>%

add_model(rf_spec) %>%

add_formula(medv ~ .)

# Fit on training data

rf_fit <- rf_workflow %>% fit(data = boston_train)Now evaluate performance on the held-out test set.

# Generate predictions

rf_preds <- predict(rf_fit, boston_test) %>% bind_cols(boston_test)

# Evaluate

metrics(rf_preds, truth = medv, estimate = .pred)Comparing models

One of the best things about tidymodels is how easy it is to swap models in and out. Here we run a plain linear regression on the same Boston data and compare RMSE directly — same workflow, different model spec.

# Linear regression on Boston data

lm_boston_spec <- linear_reg() %>% set_engine("lm")

lm_boston_fit <- workflow() %>%

add_model(lm_boston_spec) %>%

add_formula(medv ~ .) %>%

fit(data = boston_train)

lm_boston_preds <- predict(lm_boston_fit, boston_test) %>% bind_cols(boston_test)

# Compare RMSE

rf_rmse <- rmse(rf_preds, truth = medv, estimate = .pred)$.estimate

lm_rmse <- rmse(lm_boston_preds, truth = medv, estimate = .pred)$.estimate

cat("Random forest RMSE:", round(rf_rmse, 2), "\n")

cat("Linear regression RMSE:", round(lm_rmse, 2), "\n")The random forest will typically outperform linear regression on this dataset — it captures non-linear relationships between neighbourhood characteristics and home values that a straight line cannot.

As we see, our randomForest model performed much better, with a RMSE of 2.96 compared to 4.58.